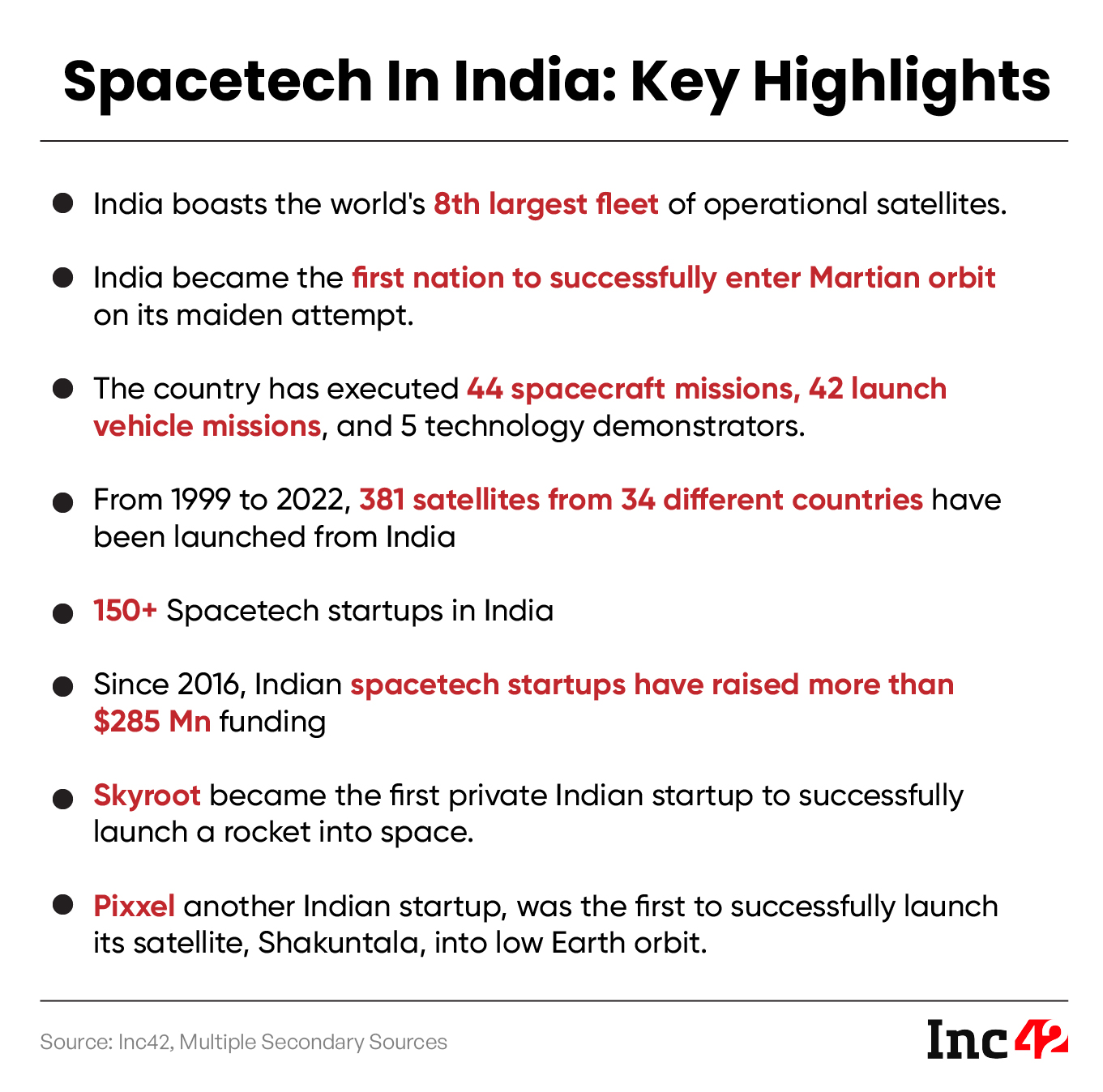

The valuation of Skyroot Aerospace at the unicorn threshold following a $60 million Series B round is not merely a milestone for a private firm; it is a structural validation of India’s privatized space trajectory. This capital injection, led by GIC, signals a shift from subsidized state-led exploration to a commercially viable launch-as-a-service model. The underlying thesis rests on the compression of launch costs through additive manufacturing and the exploitation of a geopolitical vacuum in the small satellite launch market.

The Triad of Competitive Advantage in Small-Lift Launch Vehicles

Skyroot’s strategic positioning depends on three distinct technical and economic pillars that differentiate it from heavy-lift incumbents like SpaceX or the state-run ISRO (Indian Space Research Organisation).

1. Cost Function Optimization via Additive Manufacturing

Traditional aerospace manufacturing relies on subtractive processes—machining parts from large metal billets—which results in high "buy-to-fly" ratios and significant material waste. Skyroot’s Vikram series utilizes 3D printing for engine components. This reduces the part count of a rocket engine from hundreds of individual components to a few integrated structures.

The economic implication is a reduction in the capital expenditure required for engine assembly and a faster iteration cycle. By printing engines, the firm bypasses the need for massive fixed-tooling investments, allowing the production line to remain elastic. This elasticity is critical when scaling from the Vikram-S (sub-orbital) to the Vikram I, II, and III orbital configurations.

2. The Solid-Liquid Hybrid Propulsion Strategy

Skyroot employs a nuanced propulsion mix. The Vikram I utilizes solid-fuel stages for its initial boost. Solid motors are essentially high-thrust "batteries" of kinetic energy; they are simpler to store, require no complex turbopumps, and can be integrated quickly.

However, solid fuel lacks the restart capability and precision of liquid propulsion. Skyroot’s Raman engine—named after the Nobel laureate C.V. Raman—fills this gap as a liquid-fueled upper stage. This hybrid architecture solves a specific logistical bottleneck: small satellite operators need precise orbital insertion (bus delivery) which solid boosters cannot provide alone, but they also require the low-cost, high-readiness capability that only solid motors offer for the first stage.

3. Rapid Mobilization and Launch Autonomy

The Vikram series is designed for "anytime, anywhere" launch. Unlike heavy rockets that require months of pad preparation, these vehicles use mobile launchers. This decouples the launch schedule from the congestion of fixed spaceports. In an era where "mega-constellations" require constant replenishment of failing satellites, the ability to launch within weeks rather than years is a premium service.

Market Dynamics and the Geopolitical Gap

The $60 million funding arrives at a moment of profound realignment in the global launch market. The demand for Small Satellite Launch Vehicles (SSLVs) is projected to grow exponentially as telecommunications, earth observation, and IoT (Internet of Things) firms move away from large, multi-ton geostationary satellites toward Distributed Space Systems (DSS).

Several factors contribute to the scarcity of supply that Skyroot aims to exploit:

- The Russian Exit: The removal of Soyuz rockets from the international commercial market following geopolitical sanctions created an immediate capacity shortfall.

- The Falcon 9 Ride-share Constraint: While SpaceX offers low prices per kilogram, their "Transporter" ride-share missions are like public buses—they go to a specific orbit on a specific schedule. Small satellite operators often need a "taxi" service to reach precise sun-synchronous or polar orbits.

- The Cost-of-Access Floor: European and American small-launch startups face high labor and overhead costs. Operating out of India allows Skyroot to maintain a lower burn rate while accessing a deep pool of engineers trained within the ISRO ecosystem.

The Mechanics of the Series B Valuation

A $60 million round led by a sovereign wealth fund like GIC is a bet on the "Space 2.0" regulatory environment in India. The creation of IN-SPACe (Indian National Space Promotion and Authorization Centre) acted as the de facto "single window" clearinghouse, removing the legal ambiguity that previously throttled private space investment in the region.

The valuation is built on the projected Unit Economics of the Vikram I. If the vehicle achieves its target payload capacity of roughly 480 kg to low Earth orbit (LEO), the revenue model shifts from speculative R&D to high-margin logistics.

Risk Vectors and Technical Hurdles

While the capital provides a runway, several high-friction variables remain:

- Success-to-Failure Ratios: In the launch industry, the first three orbital attempts carry a statistically high failure rate. Capital must be preserved to survive a "rapid unscheduled disassembly."

- Supply Chain Resilience: High-grade carbon fiber and specialized aerospace alloys remain sensitive imports. A shift in international trade policy could inflate the Bill of Materials (BOM) overnight.

- Regenerative Cooling Limits: While 3D-printed engines are cheaper, they must withstand extreme thermal gradients. The long-term reliability of these printed structures under high-pressure combustion is the primary engineering bottleneck.

Structural Comparison of Vikram Launch Vehicles

| Feature | Vikram I | Vikram II | Vikram III |

|---|---|---|---|

| Payload (LEO) | ~480 kg | ~595 kg | ~815 kg |

| Propulsion | Solid/Liquid Hybrid | Cryogenic Upper Stage | Heavy Lift Solid Boosters |

| Primary Use Case | Small Sat Constellations | Deep Space/High Orbit | Multi-Payload Deployment |

The Orbital Logistics Value Chain

Skyroot is not just building a rocket; it is building a node in a larger orbital economy. The funding will likely be diverted into "Stage 2" of their growth: the transition from engine testing to mass production. This requires a shift in organizational focus from "Engineering Innovation" to "Supply Chain Management."

The firm must solve the "Empty Payload" problem. Every gram of unused capacity on a rocket is lost revenue. Consequently, Skyroot’s strategy must involve an aggressive sales arm capable of aggregating diverse payloads—ranging from university research cubesats to commercial imaging sensors—into a single launch manifest.

Capital Allocation and Scalability

The $60 million will be deployed across three high-priority sectors:

- Talent Acquisition: Siphoning senior propulsion and avionics experts from global aerospace hubs.

- Infrastructure: Building proprietary test stands and integration facilities to reduce dependence on ISRO’s shared infrastructure.

- The Vikram II Development: Moving toward cryogenic engines (liquid hydrogen and liquid oxygen). Cryogenic stages provide higher specific impulse ($I_{sp}$) than solids or standard liquids, which is necessary for heavier payloads or higher orbits. This is a significantly higher technical hurdle, requiring advanced metallurgy and vacuum-rated insulation.

The transition to cryogenics represents the bridge from being a "niche small-launcher" to a "tier-one aerospace player." It is the most capital-intensive phase of the roadmap.

Strategic Direction for the 2026-2030 Window

To solidify its status as a global contender, Skyroot must move beyond the "First Indian Private Rocket" narrative and compete on pure reliability metrics. The immediate tactical requirement is the successful orbital insertion of the Vikram I.

Investors and potential customers will monitor the "Turnaround Time"—the duration between a customer signing a contract and the payload reaching orbit. If Skyroot can compress this to under 120 days, it will capture a significant portion of the "emergency replacement" market for satellites.

The long-term play is the commoditization of the upper stage. By turning the final stage of the rocket into an "Orbital Transfer Vehicle" (OTV) that can move satellites between different altitudes, Skyroot moves up the value chain from a simple transport company to a sophisticated orbital logistics provider. This requires the development of long-duration batteries, solar arrays, and high-precision RCS (Reaction Control System) thrusters.

The capital is in place. The regulatory environment is permissive. The technical path is defined. The execution of the Vikram I orbital launch remains the singular binary event that will determine if this $60 million is a foundation for a new industrial giant or a high-priced lesson in the unforgiving physics of orbital mechanics. The company must now pivot from being a venture-backed startup to a flight-proven aerospace manufacturer where "standardization" becomes more important than "innovation."

:max_bytes(150000):strip_icc()/GettyImages-2192014718-e18efe654b3f4b769a45c8692acc5f39.jpg)