Stop crying about "functional uninsurance." The hand-wringing over high-deductible health plans (HDHPs) has reached a fever pitch, fueled by a fundamental misunderstanding of what insurance is actually for. Critics love to claim that a $6,000 deductible makes a policy useless. They argue that if you’re afraid to go to the doctor because of the out-of-pocket cost, the system has failed.

They are dead wrong.

The "failure" they describe is actually the first time in fifty years that the American healthcare consumer has been forced to look at a price tag. That isn't a bug; it's the only feature that can stop the terminal bloat of US medical spending. We’ve spent decades treating health insurance like a prepaid maintenance plan for our bodies rather than actual insurance. You don't use your GEICO policy to pay for an oil change. Why did we ever think we should use Blue Cross to pay for a sinus infection?

The Fallacy of the Functional Uninsured

The term "functionally uninsured" is a linguistic trick designed to make responsible risk management look like a social catastrophe. I’ve spent twenty years watching benefits consultants and CFOs wrestle with the math of group plans. The reality is simple: low-deductible plans are just high-premium plans in a trench coat.

When you demand a $500 deductible, you aren't saving money. You are prepaying for healthcare you might not even use, while handing a 15% administrative fee to a middleman to manage the transaction.

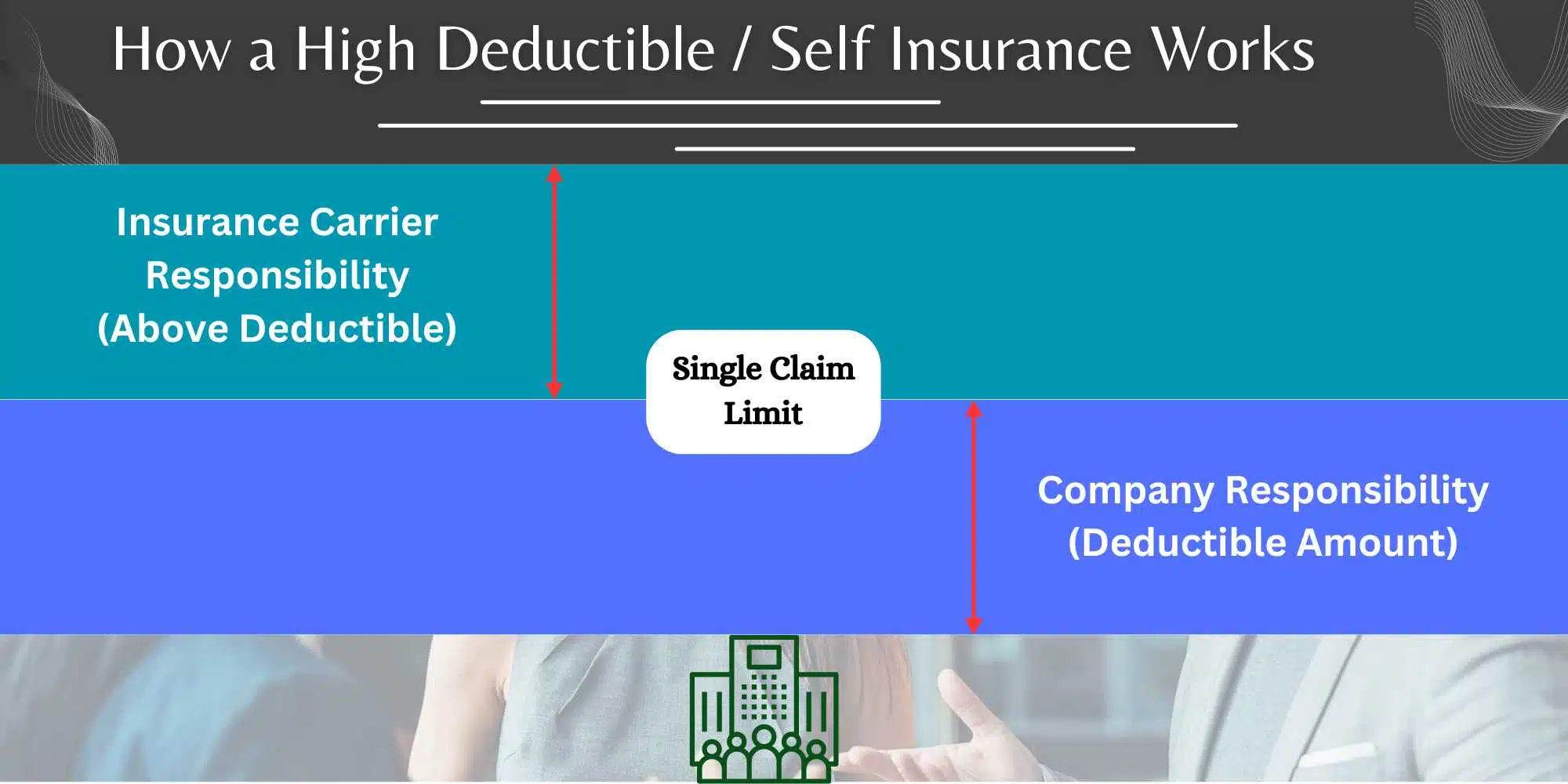

Insurance is a tool for managing catastrophic risk. It exists to prevent a $250,000 oncology bill from bankrupting your family. It is not a tool for socialized sneezing. By shifting the first few thousand dollars of risk to the consumer, HDHPs do something vital: they introduce "skin in the game."

When the patient pays, the patient asks questions.

- "Do I really need this MRI today?"

- "Is there a generic version of this?"

- "Can we do this as an outpatient procedure?"

The moment those questions are asked, the hospital's ability to charge $50 for a Tylenol evaporates. The "functionally uninsured" are actually the only people in the country holding providers accountable for their insane pricing.

The Health Savings Account is a Stealth Wealth Weapon

The loudest critics of high deductibles conveniently ignore the Health Savings Account (HSA). This is the single most potent tax-advantaged vehicle in the Internal Revenue Code, and it is only available to those with "bad" insurance.

Let’s look at the math. An HSA offers a triple-tax advantage:

- Contributions are 100% tax-deductible (lowering your taxable income).

- The money grows tax-free.

- Withdrawals for qualified medical expenses are tax-free.

If you are 30 years old and you max out your HSA instead of paying a massive premium for a "Platinum" PPO, and you invest that money in a simple S&P 500 index fund, you aren't "functionally uninsured." You are building a six-figure war chest that will cover your healthcare in retirement—the exact period when you will actually need it.

The "insured" people with $0 deductibles are burning that capital every month. They are transferring wealth to insurance company shareholders in exchange for the "peace of mind" of not having to pay $150 for a doctor’s visit. That isn't a healthcare strategy; it's a math error.

Why "Access" is a Red Herring

The common argument is that high deductibles "deter necessary care." This is a half-truth wrapped in a fallacy.

Yes, if you have to pay $200 for a visit, you might skip a check-up for a mild cough. But the data from the RAND Health Insurance Experiment—still the gold standard in this field—showed that while cost-sharing reduced the use of services, it had no significant impact on the health outcomes of the vast majority of participants.

We are over-medicalized. We treat every minor ailment as a crisis because we’ve been trained to think healthcare is "free" at the point of service. When it’s free, demand is infinite. When demand is infinite, costs skyrocket.

The high deductible is the only brake pedal we have left.

The Downside No One Admits

I’m not suggesting this system is perfect. If you are living paycheck to paycheck, a $3,000 deductible feels like a mountain. But the solution isn't to lower the deductible for everyone and hide the cost in higher premiums that eat your raises.

The real problem is price transparency.

The only reason a high deductible is scary is because you don't know if that procedure will cost $500 or $5,000 until the bill arrives three months later. Instead of fighting for "lower deductibles," we should be fighting for "binding price quotes."

If I can see the price of a flight to London in three seconds, I should be able to see the price of a colonoscopy. The high-deductible movement is the only thing forcing hospitals to finally digitize their price lists. They aren't doing it to be nice; they're doing it because patients are finally standing at the front desk with their own credit cards, refusing to sign a blank check.

Stop Buying the "Platinum" Lie

If you are a healthy professional choosing a low-deductible plan, you are making a massive strategic mistake. You are choosing a guaranteed loss (high premiums) over a potential risk (the deductible).

Consider this: In most corporate environments, the difference in premium between a PPO and an HDHP is roughly $2,000 to $4,000 a year. If your deductible is $3,000, and you don't have a major health event this year, you just handed $3,000 to an insurance executive for nothing.

If you take that same $3,000 and put it in your HSA, you keep it. Even if you get sick and hit your deductible, you’re often still ahead because you paid for it with pre-tax dollars.

The End of the Prepaid Era

The era of the "all-you-can-eat" healthcare buffet is dead, and it should stay dead. It nearly bankrupted the American economy.

The shift toward high deductibles isn't a sign of a failing system; it's a sign of a system finally attempting to contact reality. It forces us to act like customers instead of patients. It forces providers to act like businesses instead of monopolies.

If you want to fix healthcare, stop asking for lower deductibles. Start asking why the MRI costs $2,000 in the first place. Until you have to pay for it, you’ll never care about the answer.

Move your money out of the insurance company’s pocket and into your own HSA. Buy the "bad" insurance. Fund the account. Then, for the first time in your life, start acting like you own your health.

The "functionally uninsured" aren't the victims of the system. They are the only ones with the power to break it.