The financial press spent this morning obsessing over the Federal Reserve’s latest tea-leaf reading and Micron’s earnings report as if these events are the primary drivers of long-term value. They aren't. They are noise designed to keep you clicking while the actual structural shifts in the economy happen in the dark. If you are waiting for a "dovish pivot" or a "soft landing" to validate your investment strategy, you have already lost the game.

The "Morning Squawk" consensus is built on a fundamental misunderstanding of how the modern economy functions. It treats the Fed as an omnipotent deity and earnings beats as proof of health. Both are illusions.

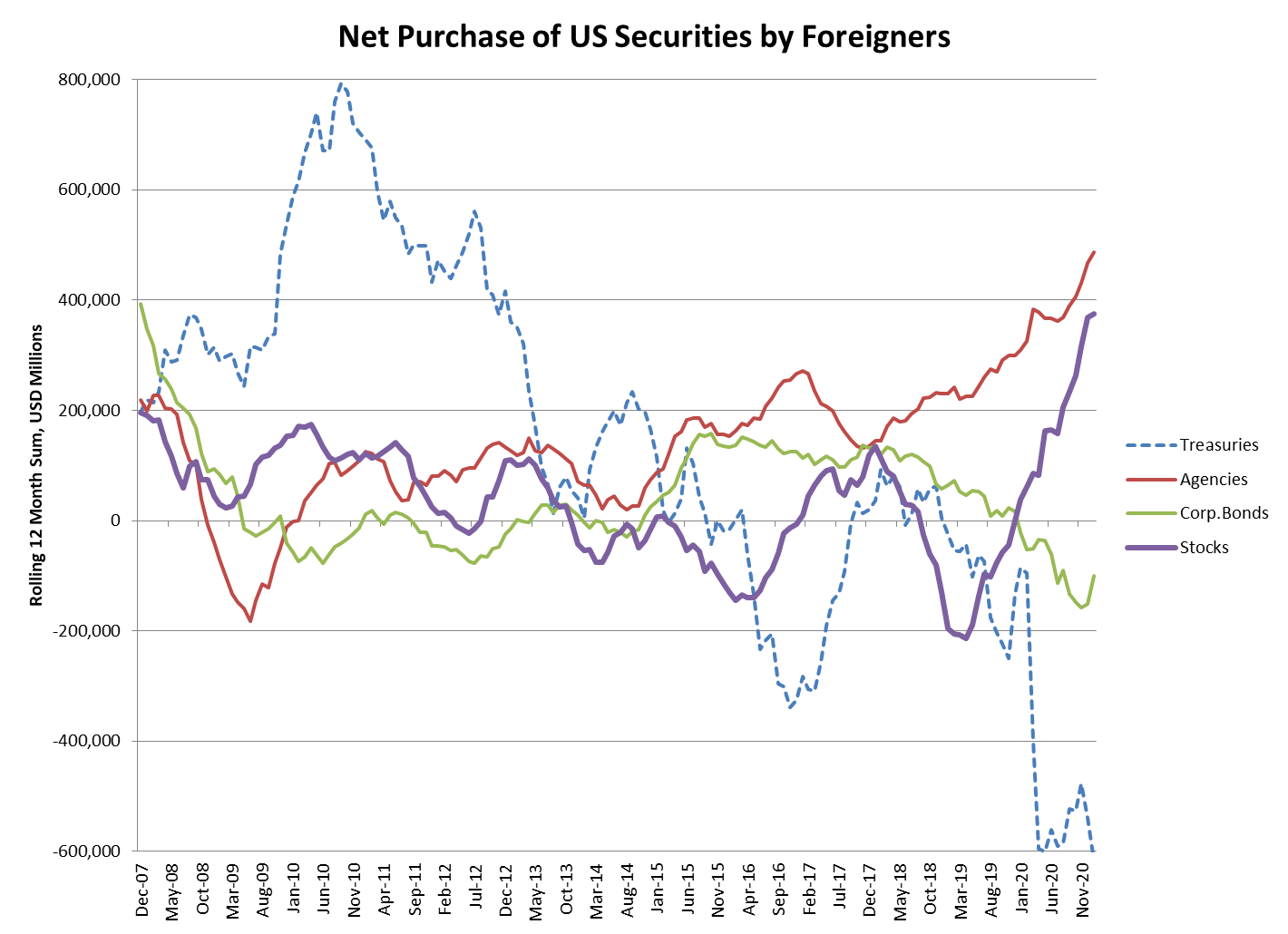

The Fed Does Not Control the Economy

Mainstream analysts treat Jerome Powell’s every syllable as a direct command to the markets. This is the "Fed-Speak Delusion." In reality, the Federal Reserve is a reactive body, constantly lagging behind the actual cost of capital and the velocity of money.

When the Fed cuts rates, it isn't "supporting the market." It is admitting that the plumbing of the financial system is already leaking. I have seen traders lose millions trying to front-run a rate cut, only to realize that by the time the cut arrives, the damage to consumer demand and credit availability is irreversible.

The real metric you should be watching isn't the Fed Funds Rate. It is the liquidity spread between private credit and public debt. While the "Squawk" crowd talks about 25 basis point moves, the private credit market—now a multi-trillion dollar shadow banking system—is repricing risk at a rate the Fed can’t touch. If you’re looking at the Fed to tell you if the economy is healthy, you’re looking at a speedometer while the engine is on fire.

Micron and the Semiconductor Fallacy

The "consensus" view on Micron’s earnings usually revolves around the "AI supercycle." It’s a lazy narrative. Yes, HBM (High Bandwidth Memory) is in high demand. But the market ignores the cyclicality of the underlying commodity.

Memory is not software. It does not have recurring revenue or "moats" in the traditional sense. It is a brutal, capital-intensive arms race. Micron’s success is currently tethered to a handful of hyperscalers—Amazon, Google, and Microsoft—overbuilding data centers.

What the analysts miss is the CapEx Cliff. Imagine a scenario where the ROI on generative AI fails to materialize for mid-sized enterprises within the next eighteen months. Those hyperscalers will stop ordering. The "unlimited demand" for memory will evaporate overnight, leaving Micron with billions in specialized inventory that nobody wants.

The industry insider truth? Micron isn't an AI play; it’s a high-stakes bet on the physical limits of power consumption in Northern Virginia and Iowa. If the power grid can’t support the chips, the chips don't sell.

The Amazon-USPS Contract Is a Subsidy, Not a Win

The headlines are buzzing about Amazon’s evolving relationship with the USPS. The "lazy consensus" says this is a win for Amazon’s logistics efficiency. It isn't. It’s a tactical retreat.

Amazon is offloading the most expensive, least efficient "last mile" deliveries to a government-subsidized entity because their own internal logistics costs have hit a ceiling. Shipping a package to a rural zip code costs Amazon significantly more than the prime membership is worth. By leveraging the USPS, Amazon is effectively socializing its delivery losses.

- The Myth: Amazon is a logistics company that happens to sell things.

- The Reality: Amazon is an advertising and cloud company that uses a loss-making delivery network to lock in customer data.

When you see "Amazon expands USPS contract," read it as: "Amazon can no longer afford to deliver to your doorstep at current margins."

The Search for "Certainty" Is a Tax on Your Wealth

People also ask: "When will the market stabilize?"

This is the wrong question. Stability is an anomaly. The period between 2010 and 2020, characterized by zero interest rates and low volatility, was a historical freak show. We are returning to a period of structural volatility.

In this environment, "diversification" into standard ETFs is a recipe for mediocrity. If you own the S&P 500, you are heavily concentrated in five or six companies that are all betting on the same AI outcome. That isn't a hedge; it’s a bottleneck.

Instead of seeking certainty, you should be seeking antifragility.

- Short the Consensus: If every "Squawk" guest is bullish on the same three stocks, the exit door is already getting crowded.

- Watch Energy, Not Interest: The ability to compute is limited by the ability to cool and power. The real winners of the next decade aren't the chip makers; they are the companies that own the copper, the uranium, and the transformers.

- Ignore the "Pivot": Even if the Fed drops rates to zero tomorrow, the inflation of the last three years has permanently reset the floor for labor and raw materials. Margins are going to be squeezed regardless of what Jerome Powell says.

The Brutal Truth About "Earnings Season"

Earnings season is a theatrical performance. Companies "beat" estimates that they helped analysts set three weeks prior. It’s a choreographed dance to prevent a sell-off.

The real data is buried in the Statement of Cash Flows, specifically the "Changes in Working Capital." If a company is reporting record "Adjusted EBITDA" while their accounts receivable are ballooning, they aren't growing. They are struggling to get paid.

Micron, Amazon, and the rest of the tech giants are masters of this accounting alchemy. They use share buybacks to mask stock-based compensation and "one-time charges" to hide recurring failures.

Stop listening to the "Morning Squawk." They are paid to keep you looking at the stage while the stagehands are stealing the furniture. The Fed is a distraction. Earnings are an edit. The only thing that matters is the cold, hard reality of energy constraints and the actual cost of non-subsidized credit.

Stop asking what the Fed will do and start asking what happens when the subsidies run out. That is where the real money is made.

Get out of the consensus before the consensus realizes it's wrong.